On Tuesday, a large ether (ETH) trade involving call options expiring in June and September crossed the tape on Deribit, sparking discussions in the trading community about the nature of the flow.

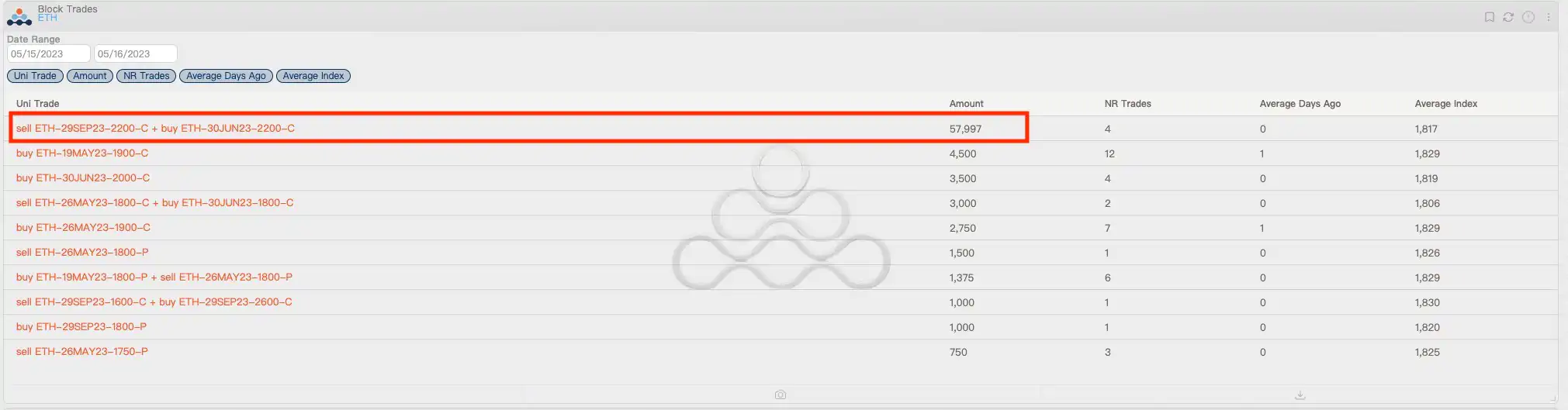

Per data tracked by Amberdata, On Tuesday, a single entity booked a large block trade that involved the purchase of over 57,000 contracts of ether's June expiry call option at the $2,200 strike price and the sale of an equal amount of contracts of September expiry call at $2,200.

Singapore-based options trading giant QCP Capital was the market maker for the trade processed over the counter (OTC) and reported to Deribit. Block trades are large transactions negotiated outside of the open market to ensure minimum impact on prices and are considered a proxy for institutional activity.

Tuesday's block traders in ether options (Amberdata) (Amberdata)

A bet on volatility?

According to Luuk Strijers, chief commercial officer at Deribit, the bi-legged trade represents a "short call calendar spread" strategy designed to make money from a large ether price move away from the spread's strike price, i.e., $2,200.

"This week, a large ETH calendar spread of almost 60k contracts was traded OTC and reported to Deribit via our block trade tool. The investor most likely expects volatility to increase or the price of ETH to increase after the June expiry, which are the key reasons to trade calendars," Strijers said.

Expectations for price turbulence in ether, as measured by Deribit's ether volatility index, recently hit a record low. Volatility is said to be mean reverting. Thus, unusually low readings often have traders betting on mean reversion or setting strategies that benefit from renewed wild price swings.

A trader with a short call calendar spread is not without risks and could, in theory, suffer an unlimited loss if the underlying asset remains steady.

The alternative view

Per Griffin Ardern, a volatility trader from crypto asset management firm Blofin, the block trade processed OTC does appear like a calendar spread at first but could be a "rollover" of a "covered call" strategy from June expiry to September expiry.

The covered call strategy involves selling a call option against a long position in the spot market, allowing coin holders to generate additional income. The strategy is taken when holders do not expect a significant price rally in the near term. A rollover means carrying forward the options position, in this case, a short call, from the near-term expiry to contracts with longer expiry.

The covered call trader instantly receives a premium or compensation for selling a call option and for being obligated to deliver shares to the call buyer at a set price on or before the option's expiry date. The trader retains the entire premium received if the underlying asset remains below the strike price at which the call is sold. The premium retained constitutes extra income on top of the spot market holding. If the underlying asset rallies, the entity is hedged since it has effectively locked in the sale price of the stock by selling a call option, but misses out on extended rallies.

Per Griffin, the market participant, an ETH holder, likely set up a covered call strategy sometime early this year by selling June expiry calls at $2,200. On Tuesday, the trader bought back the June expiry calls and sold September expiry calls, effectively rolling over or moving the covered call position to far-month expiry.

"It looks as though the entity sold a calendar spread, but actually, it rolled over a covered call," Ardern told CoinDesk. "After the trade, open interest in the June expiry $2,200 call decreased while open interest in September expiry increased, which means the trader rolled over the position from June to September."

Open interest refers to the number of open options positions at a particular strike price.

"Judging from the behavioral characteristics of this trader, he should be a whale holding coins, most likely a miner," Ardern added.

Markus Thielen, head of research and strategy at Matrixport, voiced a similar opinion, saying the strategy could generate double-digit returns in annualized terms.

"It could be a fund or someone naturally long," Thielen told CoinDesk. "I probably get 15% to 20% annualized by selling covered calls."

Note that selling or writing calls, whether as a standalone (naked) position or against coin holdings, represent a bearish view on volatility. Options are hedging instruments and demand for options depends on the degree of historical and expected price turbulence.

Selling volatility is fast becoming a preferred source of yield in the crypto market, according to QCP Capital.

Recommended for you:

- File-Sharing Service WeTransfer Partners With Blockchain Platform Minima on Mobile NFT Solution

- Web3 Community Platform Console Launches Beta to Fix 'Broken' Social Networks

- Celsius Debtors Release Sale Plan, Choose NovaWulf as Plan Sponsor

"With the collapse of the borrowing and lending markets in crypto last year, selling volatility has become a robust source of yield. We’ve seen interest to sell covered calls or puts structurally to earn yields. In this approach, investors earn a yield on assets, but the option seller takes on the risk of the option getting exercised," QCP Capital told CoinDesk.

Edited by Parikshit Mishra.